Customers who believe that they were mis-sold a top-up or guarantor 1 plus 1 loan will be able to claim any interest paid plus an additional 8% compensatory interest. To be eligible for such a reclaim you must have struggled to pay back the initial loan or have had to rely on top-up loans to pay of the original lending. Your loan lending duration must also have been between 12 and 60 months.

Following a recent influx in claims for payday loans from the likes of lending giants such as Wonga, refunds which have seen millions of pounds reclaimed by previous customers. Under strict direction of the FCA, guarantor lenders must be willing to refund the customer all interest paid plus 8% interest – provided that they can prove the loan was mis-sold.

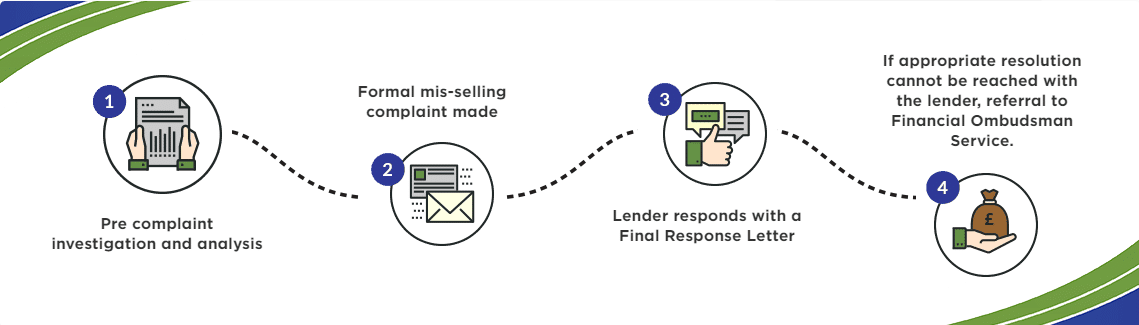

Working with our partners at Allegiant Finance Services, we will package up your compensation claim and send this to 1 Plus 1 Loans – Lenders are required to respond within 8 weeks (or sooner).